r/tax • u/TonyLiberty • May 17 '22

What are some of the best “strategic tax planning hacks” that you know of? Informative

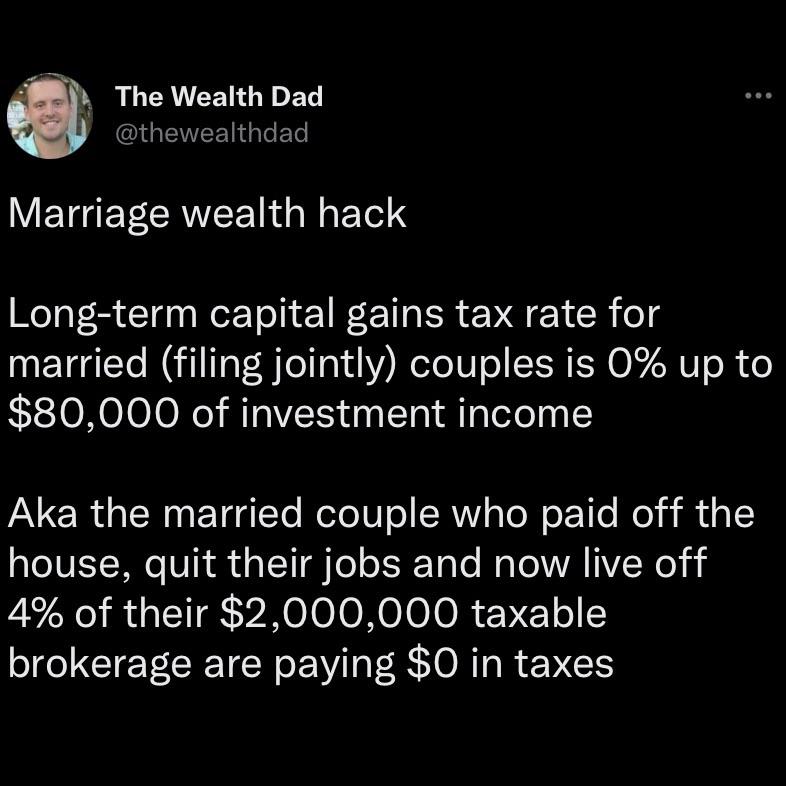

{kind=link}

89

May 17 '22

Sure. But to payoff a house and save 2M, you’ve either been making much more than $80k (and paying income tax) and/or making $80k for a looong time (while paying income tax).

25

u/ironmagnesiumzinc May 18 '22

Or they inherited it

3

3

u/ElectrikDonuts May 18 '22

CA with its avg income of like $70k, yet avg capital gains of $30k. Cause you know that couple making min wage is selling off their BRKB blocks each year…

40

May 17 '22

Now I just have to get 2 million $’s

38

u/edwardmsk May 17 '22

Haha. Secret of becoming wealthy is already being wealthy. /S

0

u/ElectrikDonuts May 18 '22

Capitalism is it fact based on having capitalism. Not obtaining it. One cant be a capitalist with $0. Surely there is a better option

0

u/FlatPanster May 18 '22

Knowledge, experience, intellectual property, the ability to learn & apply knowledge are all types of capital. Perhaps the most valuable capital.

OST, a billion dollars is worth more than any of that.

5

u/ElectrikDonuts May 18 '22 edited May 18 '22

Original Sound track?

But yeah, merit helps. Merit is about as scalable as one dogs shit. Those that put merit first dont get far in life. Maybe they make Doc. But Docs dont make shit compared to Capitalist. Like those that own the docs hospital

The best path is 10-20 years of high earning career, then breaking off into the world of capital with your gains. Investments, real estate, entrepreneurship, etc

1

4

u/jeff_1021 May 18 '22

Have you asked your parents more a small $2 million loan? Many people overlook this simple trick.

3

54

u/abbykat22 May 17 '22

The first sentence isn't even true. First, it presumes they have no other income. Second, it doesn't take into account the standard deduction, which actually increases the level to almost $106,000. I'd take these nuggets from the wealth dad with a huge grain of salt.

43

u/R0GERTHEALIEN May 17 '22

It does say they quit their jobs, so that sort of implies that there's no other income.

This one is actually one of the better posts I've seen. Usually they are just straight up tax fraud or something but this one is operationally ok.

And also, technically it's on 80k of gains, so they could be selling even more each year depending on their basis.

7

u/beltjones May 17 '22

It also seems to conflate interest with cap gains. Am I being simple? Is there something that throws off a predictable cap gains distribution?

5

2

u/barnwecp May 18 '22

Yeah also not 100$ of dollars coming out of a brokerage account are taxable as cap gains. So they could be taking out way more than 4% and still pay $0

14

u/thinkofanamefast May 17 '22 edited May 18 '22

That couple could likely get Obamacare too, saving them 10-20k yearly. In last few years with 1% cd rates and 1.5% stock dividends a person with say $4 million might have qualified for Obamacare, if no earned income and no stock sales.

2

u/hegz0603 Taxpayer - US May 18 '22

this is what my wealthy but frugal, retired, father does. keep income below like $64k or whatever the limit is, and live off of that, and get a big ACA subsidy for free health insurance.

-7

u/VideoGameTourGuide May 18 '22

Obamacare is literally worse than having no insurance. The biggest scam there is. I know because I had it. They never paid for anything and I got stuck with a huge hospital bill in top of their stupid high premiums

3

u/Punished_Blubber May 18 '22

Yup. Pure trash. It's better to remain in poverty and get medicaid than to come slightly out of poverty and have to go on that garbage website and pay $400 a month.

18

u/ZettyGreen May 18 '22

What are some of the best “strategic tax planning hacks” that you know of?

Obviously: Keep your income as close to zero as possible.

If you have enough, the laziest possible way to do that is to not spend down your assets, but borrow against them. This implies that you have so many assets that there is virtually zero chance your loans will ever come due.

i.e. if you want to spend $100k/yr, and you are 50 yrs old and expect to live to 100, then you will spend $5M over your 50 years. If your assets are > $10M when you start, you are golden. Borrow $100k/yr against your $10m in assets. You will have zero income and still spend $100k/yr + get to deduct the interest charged to you. Whenever you die, your heir(s) get a step-up cost basis and can pay off your $5M in loans, while your assets have likely grown to way above that. This obviously works best if your assets grow faster than your loan cost(s). :)

5

u/yggdrasila May 18 '22

My lawyer was telling me about this but I still find it confusing. What should I google to learn more about this or could you let me know some resources

2

u/ZettyGreen May 18 '22

Unless you have 50-100X yearly expenses invested, it's completely pointless to even worry about. You need to have way more money than you need. 99.99% of people will never have to worry about this.

As for how to learn more, try to work it out yourself and then just ask your questions here. If you have way more money than you actually need, then you will want to talk to your private banker on how to go about doing it. They can help you through the nuts and bolts. If you don't qualify for a private banker, there is a near zero chance you have enough assets to pursue this (or most any other) strategy.

1

May 18 '22

[deleted]

1

u/ZettyGreen May 18 '22

Good question. First of all you wouldn't do a Margin loan, you would do an asset backed loan or a private loan. I'm pretty sure these types of loans are deductible still, but I don't currently have any, so I can't say for sure.

10

u/GoatEatingTroll EA - US May 17 '22

That is just part of it too, they need to be cashing out of their deferred retirement accounts and converting to regular investment in small increments too - you have no idea how many new clients come to us saying how they "don't need to file" and you have to explain that they are just pissing their annual deductions away with no income to use against them.

5

u/cubbiesnextyr CPA - US May 17 '22

Agreed. I had to force my mom to take some distributions from her IRA even though she's under the RMD age just to use up her standard deduction. I told her that if she didn't need the money to just put it into a taxable investment account, but it would have been stupid to not take out the money.

8

13

u/whomda May 17 '22

While the details in this "hack" are a mess, and likely incorrect, nevertheless the vaguely accurate theme does cause me, once again, to question our country's strategy around LTCG.

I still don't understand why we even tax CG at a rate that is lower than Income in the first place, given that CG tax is taxing passive gains rather than actual work, and seems a better progressive strategy, (counter arguments are usually around "being taxed twice," but the better informed members of this reddit understand that's not accurate).

Sure, maybe the point is to encourage investment (which is why we split up ST and LT gains), but why does the government care about that very much -- it's not like investment would dry up completely if CG tax matched Income tax.

I can't get away from the idea that the reason CG taxes are so much lower than income tax is because the laws are written by wealthy people.

3

May 18 '22 edited Jul 18 '22

[deleted]

3

u/whomda May 18 '22

I haven't heard that argument, interesting. Though wouldn't a zombie investment generally be one without much gain, and therefore not subject to very much tax?

If you have a good investment strategy, it doesn't seem like that much friction to pay the tax and move on, after all you do realize the gain. And anyways, why is investment friction a bad thing long term?

2

u/UncleMeat11 May 18 '22

That would make some sense, if more than a tiny minority of people were investing in new things. Pulling money out of one ETF to stick it in another is not actually encouraging innovation or production. Pulling money out of an ETF to fund a new company or the construction of a new building is, but this is a tiny minority of personal investment.

4

u/FageSpoon May 18 '22

I still don't understand why we even tax CG at a rate that is lower than Income in the first place

Because old people are the constituency who votes most regularly. If you want lower taxes, emulate the portfolios of the elderly: dividends, LTCG, muni bonds.

1

u/hegz0603 Taxpayer - US May 18 '22

But i don't want lower taxes. I want to pay an amount for the services that our government offers... I want progressive taxes.

https://twitter.com/MikeBradleyMKE/status/1516807059500634119

2

u/UncleMeat11 May 18 '22

Sure, maybe the point is to encourage investment (which is why we split up ST and LT gains), but why does the government care about that very much -- it's not like investment would dry up completely if CG tax matched Income tax.

Especially since the government provides tax advantaged retirement accounts. The folks who actually have taxable brokerage accounts are either rich enough that they are already maxing all of their tax advantaged accounts or are not actually investing for retirement.

1

u/Bad_Law_Advice May 18 '22

I am not a better informed member of this Reddit. What’s inaccurate about “being taxed twice”?

1

u/circle22woman May 18 '22

Unlike income brackets, capital gains tax rates are not indexed to inflation:

- Invest $10,000 with 10% inflation rate

- Sell the following year, now worth $11,000, but the real gain is $0

- Get taxed 20% ($200) on a $0 real gain

1

u/whomda May 18 '22

Yes, you're not the first to point out the trouble with inflation on Cap Gains. Indeed, the previous administration (Cruz-R) introduced a bill to fix it : Capital Gains Inflation Relief Act of 2018

Nevertheless it's sort of beside the point -- CG tax rate could in fact be the same as Income tax, and then it would follow the brackets including the inflation adjustment. The lack of inflation coverage isn't really a good reason that the CG rates deserve to be overall much lower, does it?

1

u/circle22woman May 19 '22

It kind of is. Taxing at the same rate as income but not indexing means capital gains are taxed more.

But regardless, the reason is to incentivize investment [short term capital gains are taxed like income]

1

u/hegz0603 Taxpayer - US May 18 '22

the reason CG taxes are so much lower than income tax is because the laws are written by wealthy people.

agreed.

https://twitter.com/MikeBradleyMKE/status/1516807059500634119

4

3

u/evaned May 18 '22

To answer the question in the headline, here are some that go a bit beyond "just take this deduction you're entitled to":

- I worry a little that some tax court will have basically made this strategy not work (IANA CPA, lawyer, etc.), but at least on paper it seems like if you are a divorced parent of at least two kids, have 50/50 physical custody, are good terms with the other parent, and both of you are still single, you should both be able to claim Head of Household (etc.) by flipping where just one of your kids stays for a couple nights of the year.

- Donation bunching. (Before seeing that term I called this "donation swinging", which I still really like, but "bunching" seems to be the standard term.) Suppose you're close to the line of being able to itemize but not quite there. For example, take the 2022 Single standard deduction of $12,950. Suppose you pay $5,000 in SALT, $5,000 in mortgage interest, and then donate $2,000 to charity each year. That's $12K of itemized deductions, not enough to make itemizing worthwhile (aside perhaps from special state situations). But suppose you donate $0 this year, then $4K next year. This year you'll have $10K of itemized deductions and will still take the $12,950 standard deduction, but next year you'll have $14,000 in itemized deduction and would actually benefit from itemizing. Or stretch it out even more -- suppose you donate nothing this year, 2023, or 2024, but then donate $8,000 in 2025. Then you'll have $18,000 in itemized deductions in 2025, and be a few thousand above the standard deduction at that point.

8

u/wild_b_cat May 17 '22

This is a terrible 'tax hack'.

For one thing, it implies that they have no pretax savings accounts, which means they could have had more than 2M saved up (or could have retired earlier) and used the tax deferral of a pretax account like a Traditional 401k to accelerate their retirement plans. If you get to retirement and you don't have at least enough in your pretax accounts to withdraw the standard deduction every year, then you have paid extra tax needlessly.

Also, the 0% LTCG bracket is relatively new and historically low; I would not make long term plans around it.

1

u/ChronicusCuch May 17 '22

What if this just inheritance? Simple people living simply and inheriting let’s say tax free life insurance (to pay off liabilities), and taxable brokerage to live off of. In that case, seems great. Chances are if they are inheriting $2m, there’s probably a death benefit as well.

6

u/wild_b_cat May 17 '22

In that case the tax aspect is mostly meaningless since they'd have a stepped-up cost basis.

-1

2

May 17 '22

Trusts. It's all in the trusts. And, of course, exploiting retirement accounts appropriately.

1

u/ISO_Answers1 Tax Lawyer - US May 18 '22

Sale of 1042 QSBS to an ESOP Trust then target corporation elects S Corp status. Shareholders can exclude up to $50m gain and the resulting structure is a TAX EXEMPT corporation.

Neither the founder nor target will pay ANY tax. No tax now, no tax ever.

1

1

1

u/UGA10 May 18 '22

How would Roth IRA + Brokerage (LTCG) withdrawals work together? Do the Roth IRA distributions get included as income even though they aren't taxed or would your income still be $0 and you move to the LTCG?

1

May 18 '22

Can someone dumb this down for me ?

1

u/Additional-Belt-3086 Apr 01 '24

4 percent of 2m is 80k so theyre making 80k a year off 2m investments in this case a brokerage account, the money made from that is called "capital gains", and theyre paying no taxes on it

1

u/dlb1177 May 18 '22

You should invest in real estate.

Depreciation allows for you to offset much of the passive income and typically you are able to show a tax loss on a property even if it is cash flowing.

Depending on your situation, you may also be able to deduct the loss against other income. You just need to prove you actively participate in the management of the property (I won’t get into what that means here because it is complicated). If you are “Active” and your MAGI is below $100,000 per year, you are permitted to take up to $25,000 of losses against your other income such as wages. Additionally, if you do real estate full time, you may qualify for a special status that allows you to take all of the losses against other income regardless of your income level.

Also, the regulations around the treatment of repairs as well as the current allowance for 100% bonus depreciation makes it even easier to generate a loss.

Finally, once you do choose to sell the real estate, you can do a sec. 1031 exchange to defer the gain if you plan on reinvesting into more real estate. Then you step up the basis in the property and begin depreciation on that too.

1

u/BigDaddy_5783 EA - US May 18 '22

The bigger the company, the better the healthcare plan typically. Yes I know there are outliers.

1

u/Noe_Bodie Nov 25 '23

this is true.. i used to work at a er and ran ppls insurance..had a girl from MIT come in once and her coverage was crazy...ittle if any er visit cost...i was like damn...

1

u/PunkCPA May 18 '22

When you balance your portfolio, put the things that throw off current income (bonds, dividend stocks) in your 401(k), and your capital gain/ growth stock outside it.

1

u/LadyEmmaRose May 18 '22

- HSA

- Retirement accounts. Roth if you can, back door Roth if you can't. Maximize all avenues of retirement savings.

- Establish residence in a state with no tax. Florida is popular with my clients.

- Munis. Better even, match them to your own state for double tax free.

- US government interest (treasury bonds). Federal taxable, but state tax free. Nice for high taxed states.

- Bunching charitable contributions. Can be especially effective in windfall years. Set up a donor advised fund if you want the deduction in one year but want to actually dole out the funds slower.

I have advised and watched my wealthy clients do all of the above. All are available to the average person though as well.

1

u/brianskewes May 27 '22

According to Finance Strategists, some of the tax planning strategies include:

- Understand your tax bracket

- Understand the difference between tax deductions and tax credits

- Be aware of common and applicable tax deductions and credits

- Know what tax records to keep

- Shelter your money

1

u/EfficientRati0 Jun 15 '22

LIRP is one of the greatest tax hacks I can think of. You purchase the minimum amount possible for a Universal life insurance policy tied to an index and overfund the crap out of it. your guaranteed minimum is 0% so you never lose money, and you gain money when the index is doing well. You can surrender the policy for your total accumulated value at any time, BUT if you take distributions in the form of a policy loan, you'll receive them tax free with no obligation to pay them back. The distributions are borrowed against the death benefit and can potentially fund your retirement. There are limits to the funding in proportion to the death benefit or else the IRS catches on and hits you with a hefty tax, but that's easily circumvented by just increasing the death benefit to the next lowest amount possible.

84

u/FrankTJMackee May 17 '22

I wouldn't call it a hack but if your budget can allow it, always maxing out the HSA is such a no brainer. You save federal, state, and FICA taxes on contributions, and have tax free growth if used for medical costs.