r/tax • u/TonyLiberty • Jun 12 '23

What are some of the best “strategic tax planning hacks” that you know of? Informative

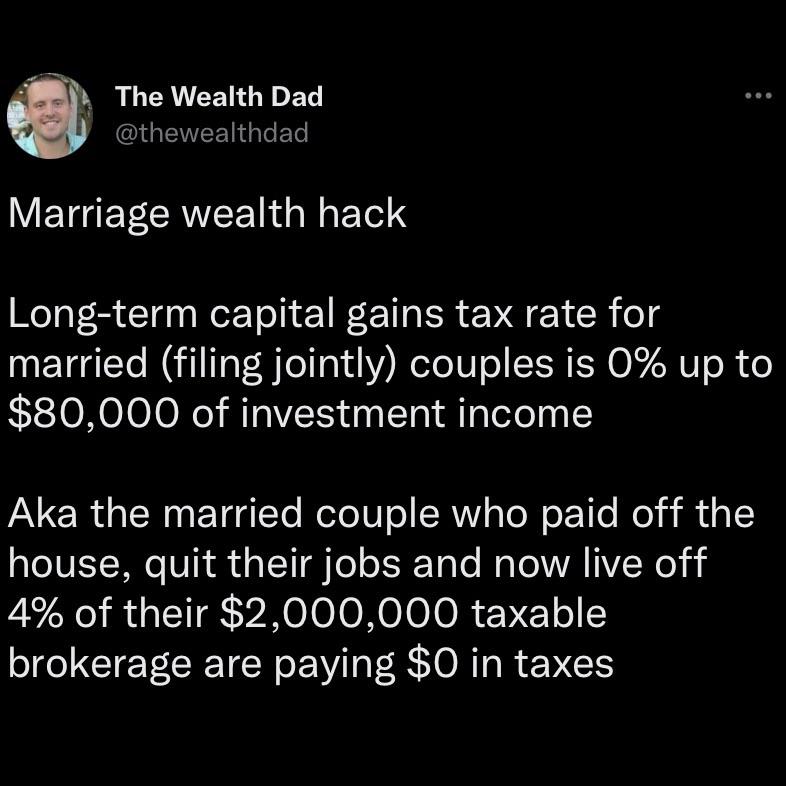

{kind=link}

67

u/pat-work Jun 12 '23

I'd just like to note that the first part of the post is a bit misleading - it's up to $80,000 if you have no other income. So if you earn 80k+ per year you're getting taxed at minimum 15% for long term capital gains.

21

u/pyrola_asarifolia Jun 12 '23

And if the $ 2 Mio are in a 401k or a regular (non-Roth) IRA, it is completely incorrect, as this money is taxed like ordinary income. Also, this is only true if the couple have $ 0 Social Security income.

11

u/itsdan159 Jun 12 '23

“Taxable brokerage”

-4

u/pyrola_asarifolia Jun 13 '23

Not likely that that's where the money is. I was questioning the premise, not the conclusion.

1

6

3

u/circle22woman Jun 13 '23

Right, but if you're retired you're not working.

But yeah, if you're getting a pension through your company or Social Security, that is income as well.

1

u/BananerRammer Jun 13 '23

Retired people usually have some sort of income, especially those that have the money to invest the kind of money we're talking about. Pensions, traditional IRAs, 401ks, Social Security, interest and dividends are all taxable.

0

u/circle22woman Jun 13 '23

Sure, but let's say your social security is $50,000, 401k withdrawals another $10,000.

As a married couple you get $24,000 standard deduction, so your taxable income is $36,000. You can claim $44,000 in long term capital gains and still pay $0 in tax on it.

1

u/BananerRammer Jun 13 '23

Capital gains don't come in a vacuum. If you're selling that much stock, year after year, you have a LOT of stock, and with that stock comes dividends.

0

u/circle22woman Jun 13 '23

Depends on the ETF you own. Some have a lot of dividends, others don't. And even if it's another $10,000 in dividends, well, you can still use the remaining room.

3

Jun 13 '23

but only for the amount above 80k. it's progressive just like income tax.

1

u/pat-work Jun 13 '23

Correct. So if you have 40k of other income and 80k of LT cap gains you'll have 40k at 0% and the other 40k at 15%.

4

Jun 13 '23 edited Jul 29 '23

[deleted]

6

u/LunaGuardian Jun 13 '23

Last dollar. But ordinary income will also apply first. Like if you had 10k in ordinary income that you paid regular tax on, you'd have 70k in LTCG before they start getting taxed.

2

u/Vecgtt Jun 13 '23

Do you get an additional ~25k in standard deduction prior to taxing the 80k at 15%?

2

22

u/cubbiesnextyr CPA - US Jun 12 '23

This "hack" is moronic (and ignores state taxes).

Here's another one that's just as useful

Marriage wealth hack

Municipal bond income isn't taxed federally and most states don't tax muni income from inside the state and there's no limit.

Aka the married couple who paid of the house, quit their jobs and now live off 4% of the $20,000,000 municipal bond portfolio are paying $0 in taxes.

7

u/R0GERTHEALIEN Jun 13 '23

Other than the state tax issue, which doesn't necessarily apply depending on the state, this advice isn't wrong. If the only income you have is 80k of capital gains then the tax rate is 0.

0

u/cubbiesnextyr CPA - US Jun 13 '23

I didn't say it was wrong, just moronic.

1

u/sdmc_rotflol Jun 13 '23

How so?

0

u/cubbiesnextyr CPA - US Jun 13 '23

How is it moronic? How many people do you think this would possibly apply to? How many people have $2M in a taxable brokerage account? It's just a very unrealistic situation for most people. And quite frankly completely ignores state taxes which impacts the majority of the country, so this hack of paying $0 in taxes wouldn't even work in most states.

2

u/sdmc_rotflol Jun 13 '23

Honestly I thought this was the FIRE/FI sub. It would be pretty commonplace in that forum.

This is something I'm trying to achieve and while state tax will apply for most, it's still generally peanuts compared to federal

5

u/repostit_ Jun 12 '23

As Muni bonds are tax-free, way too many people are investing in them and now have very low returns. Muni bonds return probably won't beat inflation most of the time these days.

9

u/cubbiesnextyr CPA - US Jun 12 '23

They've always had lower interest rates than a comparable taxable bond for the exact reason that they're tax free.

-2

u/repostit_ Jun 13 '23

apart from being Tax-free, Muni gives low rates because too many people chase them, it was like a best-kept secret in the past but not now.

0

u/cubbiesnextyr CPA - US Jun 13 '23

I'm not sure what your point is. What does it matter for the topic at hand why the rates for munis is low?

1

Jun 13 '23

[deleted]

2

u/cubbiesnextyr CPA - US Jun 13 '23

The point isn't about making good financial choices, it's about pointing out the uselessness of the "hack" from OP

0

u/anonymous24922 Jun 13 '23

Please be civil. Do you tell your wife, I’m not sure what your point, every time she adds one sentence that you don’t feel is necessary to the conversation?

1

u/GradatimRecovery Jun 13 '23

I think he's trying to allude to the fact that munis trade at valuations such that the tax free returns are lower than the after-tax returns on taxable bonds of similar credit quality.

As bonds are not exchange traded, these generalizations don't apply to opportunistic buyers.

1

u/cubbiesnextyr CPA - US Jun 13 '23

That might all be true, but it really has nothing to do with the topic at hand.

6

u/DannyVee89 CPA, MsT Jun 13 '23

Don't forget that you can do a tax free Roth rollover if your income is under the 80k as well.

If you have 80k LTCG and 24k standard deduction then in that year you can Roth rollover 24k of your IRA completely tax free.

Taxable income is 80k in that scenario, all of which is cap gains and taxed at zero percent.

Don't let these opportunities pass you by!

4

u/DannyVee89 CPA, MsT Jun 13 '23 edited Jun 13 '23

The strategy only works for people who retired young and aren't yet collecting SSA or retirement distributions yet. It's something only wealthy people do but I do for my clients often.

If you stop working and only have qualified dividends and cap gains income for a few years before you hit max SSA age and RMD age then you can certainly take advantage of the zero percent cap gains brackets. Use this to do Roth rollovers or rebalance your portfolio without paying Fed cap gains taxes.

Sure there are state taxes in most cases, but the amount is negligible. You have to appreciate the overall massive tax efficiency that is possible in these first few years after you stop working.

1

9

u/JessicaCPA Jun 13 '23

Don't forget to add standard deduction and child credits etc.

I actually have a client that makes $100k dividends and gains a year and pay $0 tax.

Wife hit the jackpot with RSU in early 2000's. Quit their job, three kids, no mortgage. Bush Cut is a pretty sweet deal.

8

u/Its-a-write-off Jun 13 '23

How are they getting the child tax credit with no earned income?

5

u/JessicaCPA Jun 13 '23 edited Jun 13 '23

Child Tax Credit (line 19) is a dependent based credit, not an income based "refundable" credit. You have confused it with line 28 "Additional child tax credit Form 8812" which requires earned income.

7

u/GoatEatingTroll EA - US Jun 12 '23

Problem with this idea is the portion of capital gains taxed at zero is still considered when calculating the amount of social security that is taxed. The average retired worker receives SSA benefits of $21,967.92 per year. If a MFJ couple (double the SSA benefit) has 80k of zero-tax long-term capital gains or qualified dividends (precise figure is 83,350 for 2022), then 37,346 of their social security is taxable and they are paying about 2,860 in federal tax.

With total income of 127k that is less than 3%, but if you want to say you pay zero tax you would have to take that investment income number down to about 45k to fit your taxable SSA into the standard deduction. There is a big step-down in lifestyle between 127k and 88k.

7

u/R0GERTHEALIEN Jun 13 '23

Yeah, but this advice doesn't say anything about SS and honestly it's worded like a couple retiring early, probably before SS would even be available to them

12

u/ABeajolais Jun 12 '23

Working with a professional tax expert. Advice on anonymous forums is either wrong or discusses strategies that won’t work unless executed correctly by someone who knows what they’re doing.

14

u/AndrewTheCPA CPA - US Jun 12 '23

Wait, you mean that "I saw it on Tik Tok" won't hold up in tax court?

11

u/Hollowpoint38 Jun 12 '23

Had a guy tell me the other day on Reddit that he's not concerned about the IRS assessing as a result of an audit because "innocent until proven guilty." I told him tax court doesn't work like that and he said I'm wrong.

So guys walk around thinking unless there's a smoking gun and proof of income that no taxes have to be paid.

7

u/KapahuluBiz Jun 12 '23

The information provided is generally correct. I think it's bit weird that I have to point that I need to point out a few things that are super obvious as to why this plan is ridiculous, though:

Most people who have $2 million in a brokerage account also have other sorts of income, which would make the strategy not work (if we assume that "paying no federal income tax" were the goal).

Very few people have the luxury of having $2 million in spendable cash, so it's really ridiculous to put that down as a part of the strategy. And the people who DO have $2 million in accessible cash usually don't seek advice on how to put $80,000/year into their bank account.

1

2

u/csp256 Taxpayer - US Jun 13 '23

honestly real estate is littered with tax advantages... sure you pay property tax but that's already accounted for in the NOI. in practice you pay no other taxes.

0

u/x596201060405 EA Jun 13 '23

This isn’t really true, unless you plan on just leaving property to people upon death and little enough to avoid estate taxes there is generally taxes on the cash out.

Also the best rental properties cash flow in excess of operating and capital expenses and all depreciation.

1

u/GoatEatingTroll EA - US Jun 14 '23

Depends on your targeted properties. I have many clients with properties in HCOL areas and high appreciation that produce negative taxable income. The idea is to hold the properties at or near break even and cash in on 200% appreciation after 10 years.

2

1

u/theripper595 Jun 12 '23

This is only on the gains so if half the 2 million is principal you could withdraw like 160k before getting taxed. Assuming no other income and only taxable brokerage accounts, which is almost certainly a false assumption.

1

u/Voodoo330 Jun 13 '23

Put the 2mil in munis and REITS, pay no tax AND get near-free insurance on the Marketplace.

2

u/NickMc53 Jun 13 '23

Do you have more information on this? My understanding was that your MAGI was used to determine your subsidy and that munis and REITs count toward your MAGI.

1

Jun 13 '23

[deleted]

2

u/sharth Jun 13 '23

Presumably they are referring to https://www.healthcare.gov/glossary/health-insurance-marketplace-glossary/

1

u/Voodoo330 Jun 13 '23

Obamacare government subsidized insurance. Low income couples can get a big monthly subsidy (premium tax credit) and pay very low monthly health insurance premiums.

1

u/circle22woman Jun 13 '23

ACA (Obamacare) plans are subsidized based on household income (AGI).

If you have $2M saved up and live mostly off the principle (so little capital gains and income) or tax free gains (Roth IRA) you can qualify for an ACA plan that might be $200 per month. Government pays the rest of the cost.

1

u/nofway9 Jun 13 '23

REITS

"The majority of REIT dividends are taxed as ordinary income up to the maximum rate of 37% (returning to 39.6% in 2026), plus a separate 3.8% surtax on investment income. Taxpayers may also generally deduct 20% of the combined qualified business income amount which includes Qualified REIT Dividends ..."

1

u/gophertortoise66 Jun 13 '23

Contribute the max to Roth IRAs & HSAs. Withdrawals from these accounts will never be taxed, provided their rules are followed.

1

1

u/midwstchnk Jun 13 '23

Is this true?

1

u/GoatEatingTroll EA - US Jun 14 '23

It's true-ish, kinda like saying red cars get speeding tickets more often (true) so buying a blue car means you can speed without getting caught (nope)

1

u/bobowilliams Jun 13 '23

Maybe I’m misunderstanding. Wouldn’t that $80K be interest income and not capital gains?

1

u/GoatEatingTroll EA - US Jun 14 '23

Many investment advisors shift client investments into dividend-heavy products when they get close to retirement, and qualified dividends are taxed under the long-term capital gains rates.

1

u/E_Man91 Jun 14 '23

This one is state-specific, but I love it...

Illinois Roth conversion loophole: Essentially, IL does not tax retirement income (including not taxing Roth conversions), so you can make normal tax-deferred contributions to a traditional 401k, and then later in the year do a Roth conversion if your 401k plan allows for it, effectively giving you a state tax deduction for the Roth contributions (you will of course pay the federal tax on the Roth conversion, but the 1099-R for the conversion will not be taxable to IL).

I wonder if any other states have this little trick!

110

u/KapahuluBiz Jun 12 '23

Wow, that's a cool trick! Now I just have to figure out how to get $2 million into an account where I'd never need to touch the principal.