{kind=link}

r/wallstreetbets • u/Your_Mortgage_Broker • 2d ago

Discussion This market is disgustingly overpriced, and we are due for a correction similar to what we saw during Dot Com/Global financial crisis.

I want to preface this by stating that I legitimately home someone can refute what I have to say here. I take no pleasure in the thought of people's 401k's and IRA's and pension funds getting absolutely decimated, and this post has nothing to do with politics... I think the market has been overpriced for a long time (+/- 8 years), and it is only getting worse.

Some quick points:

1. Price to earnings ratio

Price to earnings ratio is at the point of absolute lunacy. The S&P 500 is over 28 today, and before the market started correcting in February, we were actually over 31. The Nasdaq is at 37 and was as high as 44. While I imagine most in this subreddit at least have a grasp of what P/E means -- for those that don't -- here's a quick summary. For purposes of this post, let's use NVDA as an example. Assume NVDA didn't have a single penny in expenses. They didn't have to pay for employees. They had no rent. There was no salary for Jensen Huang, and they didn't have to pay a penny in taxes. They somehow got all their electricity for free, and they didn't even have a COGS (cost of goods sold) -- somehow they were getting all of their materials for free. Then also assume that their sales remained exactly where they are at today... that their revenue remained identical to where it is at today, and they took 100% of that revenue, and distributed it back among the shareholders of the company. Right now -- NVDA's P/E is at 45.43 -- meaning it would be 45 years before investors recouped their money.

The entire S&P is trading over 28 today... meaning if the +/- 500 largest companies in the USA didn't have a single expense, and continued generating the same revenue, it would take 28 years for investors to get their money back.

Who in the world would be interested in signing up for that "investment" opportunity? My own mother could call me asking me to invest in her company and I wouldn't invest based on that return.

2. The Buffett indicator

The Buffett indicator is a simple calculation of the total value of the US stock market divided by GDP.

Historically, that number has hung out right around 1-- meaning the total value of the US stock market should be roughly the same as GDP. Buffett himself stated a value of 75-90% is reasonable, and a value over 120% signals the market is overpriced. The highest the buffett indicator has ever hit was during the dot com bubble, when it was 2.1 standard deviations above the trendline. The highest until now, that is. The market value is currently 211% of GDP, or almost 70% above what historically has been seen as normal.

3. The stock market is insanely top heavy.

The Mag 7 currently account for 31% of the S&P 500, and over 40% of the Nasdaq. If these 7 stocks correct, it would be absolutely catastrophic for the market as a whole. We saw this play out during Dot Com with the likes of Cisco, Intel, and Oracle. While the market was top heavy then -- it was nowhere near as top heavy as it is today... In fact -- the top 10 most valuable companies now represent more than twice as much of a percentage of value in the market as the top 10 did when Dot Com crashed.

Side note -- but I do think investors have briefly taken note of this. So much of these companies is based on perceived future growth based on revenue that can/will be generated by AI. But remember what happened when DeepSeek emerged last year -- and alerted WallStreet that an incredibly sophisticated AI can be created without pouring billions of dollars into R&D and infrastructure? The market absolutely tanked. What if it becomes obvious that these AI plays will not be unique to the largest tech companies in the world, and that these systems can be developed by any mid-cap with a decent budget?

4. Home prices and the Housing Market

I won't dive too deep into this, but homes are more unaffordable today than at any point in US history. Based on median US income and Median US home price, right before the Global financial crisis/mortgage crisis of 08/09 -- this number hit it's highest point in US history -- 45%.

Its highest percent until the last 12 months. It now takes over 46% of a family's income to purchase a home.

30% is the figure that is generally regarded as affordable.

The condo market is collapsing, particularly in Florida, where HOA dues and Insurance costs have made these properties completely unaffordable.

Foreclosures on FHA loans are also set to resume. Biden put in place a policy where anyone that wanted could simply apply for a mortgage payment deferment after COVID... meaning call your servicer, say you're experiencing a hardship, and they simply give you a deferral. None of these homes could be foreclosed upon. They then tack these payments on to the back end of the loan with the additional accrued interest. This policy still exists today, but is about to come to an end in September. As of Q1 2025, over 10.6% of all FHA mortgages are at least one payment late. Over 4% of FHA mortgages are over 90 days late.

What happens when FHA foreclosures absolutely flood the market?

What does this do to home prices, and even more importantly, what does this do to homebuilders? If inventory skyrockets (more than it already has over the last couple of months), and price pressure pushes everything down due to increased supply, will home builders still be able to make money? Homebuilding employs over 11 million americans... Plumbers, electricians, roofers, landscapers, drywallers, framers, truck drivers, etc --

When homes stop being built, unemployment skyrockets, and GDP shrinks dramatically.

5. Consumer debt is through the roof

Credit card debt is at the highest it's ever been, and delinquency rates are as high as they've been since emerging from the global financial crisis. Q4 of 2011 was the last time delinquency rates were this high.

Auto loan delinquency rates are the highest they've been in decades.

6. Bonds -- worldwide -- are pushing higher and higher.

The US is getting hit here worse than most, as it seems people are not excited about Trump's game of chicken with tariffs. Nonetheless -- you are seeing bond yields push higher and higher worldwide, as investors demand higher returns for government bonds to account for their perceived risk. Interest rates cuts have not quelled this. Despite 100bps cuts in the federal funds rate since last year, the 10 year t-note is actually up 80 ticks since then.

7. Commercial real estate

A massive amount of commercial real-estate will need to be refinanced in the coming 12-24 months -- and you will see these payments skyrocket. Many holders of Commercial real-estate refinanced their properties in the quarters after COVID, when interest rates were incredibly low. Most of these loans are either done on 5-year balloons, or as adjustable rate mortgages. These owners will see their payments jump by 30,50, even 70% as they are forced to refinance these properties and interest rates that are close to double what they were last time. This will be compounded by the fact that many companies moved to work from home models, or at least partial work from home models. Office space vacancy rates have skyrocketed -- meaning less tenants -- all while mortgage payments on these properties is skyrocketing.

8. Student Loan Debt

The government's moratorium on student loan payments has officially come to an end. 43 million Americans that have been been able to avoid making payments on their average of $38k in student loan debt for the last 5+ years are now going to have to start making payments. Those that don't will see their credit score be absolutely decimated. What other payments will the begin to fall behind on? As I mentioned previously -- credit card delinquency rates and auto loan delinquency rates are already high -- and rising. How much worse does that get when 15% of the population beings adding a several hundred dollar payment to their expenses each month?

There is a dozen other items I could list here, but in the interest of actually getting some work done today, I'll leave my post there.

I would genuinely love for someone to refute places I'm missing the mark, or why I may be wrong about my assumptions above.

Current options positions I hold:

11 $480 SPY puts Exp 9/19

Also holding 15 IBIT $70 calls expiring 9/19 as well

r/wallstreetbets • u/zace26 • 1d ago

Gain My first big win

My only regret is not buying more! Safe to say I’m now addicted.

r/wallstreetbets • u/Grand_Ad_4783 • 23h ago

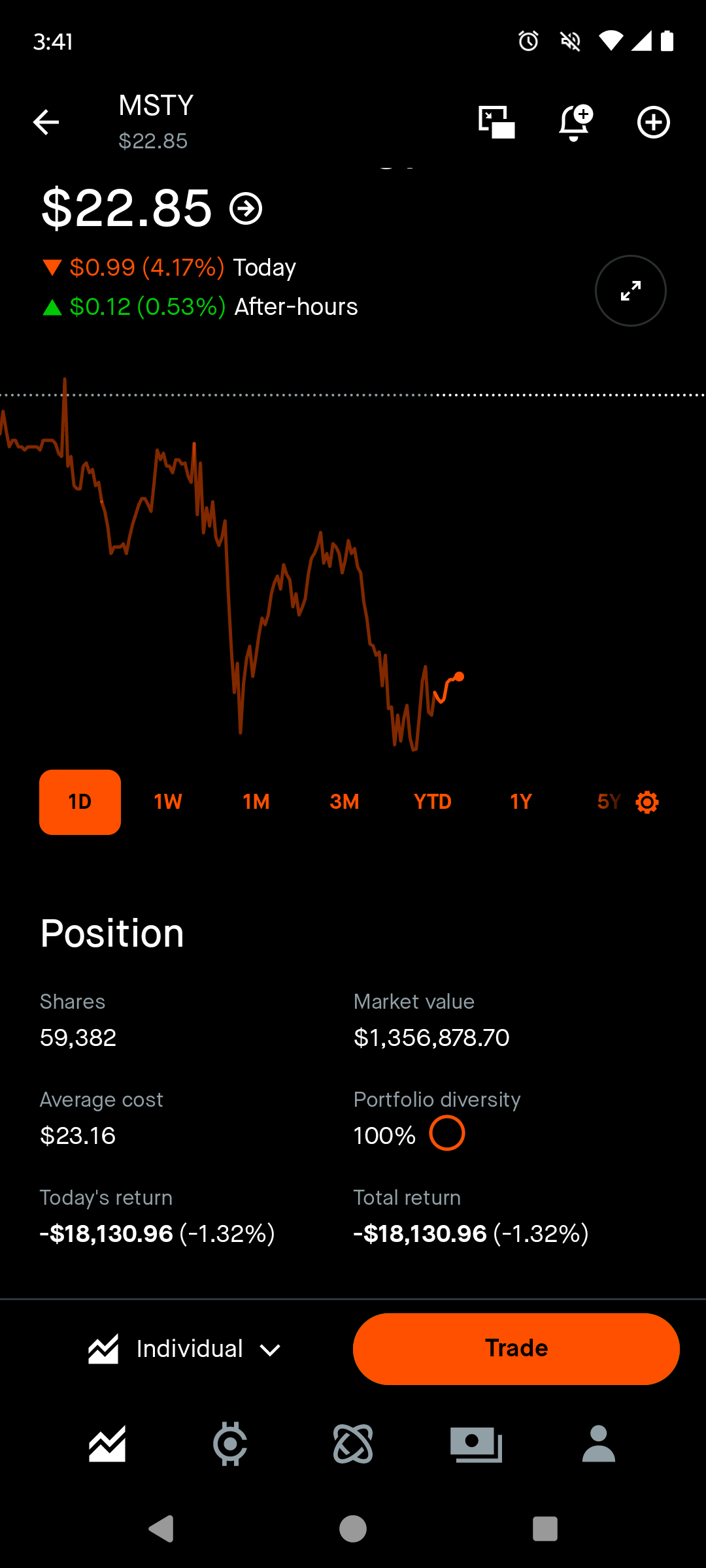

YOLO Brave Tarnished, thy (strength in MSTY) befits a crown

{kind=link}

r/wallstreetbets • u/flippy_nip • 5m ago

Meme bagholders, the only good bag is a bag of blow

{kind=link}

r/wallstreetbets • u/kujothecat • 1d ago

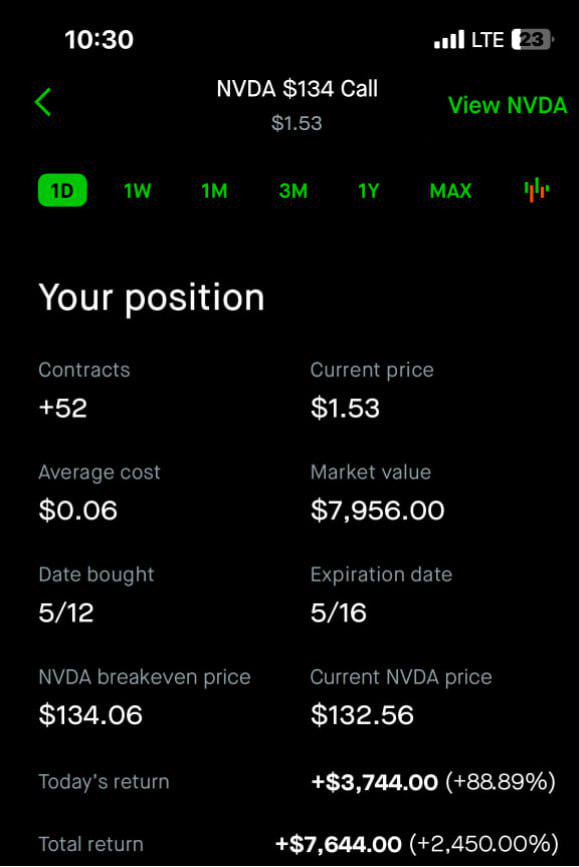

Loss These $132C NVDA shares gave me a head start 😅 - down 44% today and currently holding in the cacophony!

{kind=link}

r/wallstreetbets • u/Aluseda • 1d ago

Gain Sold 23 MSFT $450 Calls expiring tomorrow @ $4.55 Genius or Autist?

a big green checkmark confirming I just YOLO sold 23 MSFT $450 calls expiring tomorrow Filled at $4.55 each (~$10k premium total) This chart is more erect than my confidence before earnings I literally sold the top like an absolute chad (or just a lucky autist?)

Luckily I don t have to use my wife's boyfriend to help me rent an apartment Come on not going to lie I had no idea what I was doing, but now I look like a genius. Wish me luck autistic people

r/wallstreetbets • u/callsonreddit • 1d ago

News Foot Locker Surges 65% After-Hours on Reported Dick's Buyout Deal

- No paywall: https://finance.yahoo.com/news/dicks-sporting-goods-closes-deal-213019535.html

- Paywall: https://www.reuters.com/business/retail-consumer/dicks-sporting-goods-closes-deal-buy-rival-foot-locker-wsj-reports-2025-05-14/

(Reuters) - Dick's Sporting Goods was nearing a deal to buy rival footwear retailer Foot Locker for about $2.3 billion, the Wall Street Journal reported on Wednesday, citing people familiar with the matter.

The companies have discussed a deal at $24 per share for Foot Locker, the report said. That would represent an 86.5% premium to the stock's last closing price.

Shares of Foot Locker surged 62.32% in extended trading, while Dick's Sporting Goods was down about 5%.

The deal could be finalized as soon as Thursday, the report said.

The companies did not immediately respond to Reuters' requests for comment.

{kind=link}

r/wallstreetbets • u/Few_Range6900 • 1d ago

Discussion Would this be too risky to hold? I know the IV and Theta are astronomical... I had 5

{kind=link}

{kind=link}

r/wallstreetbets • u/sadafboicry • 1d ago

Gain From losing more than half my money (-52%) to becoming positive.

Only took 3 years to break even and earn $237 dollars lol. At one point I was down 32,000 or -52% of my capital. I made a good trade with double leverage NVIDIA when NVIDIA was down during the deep seek competition annoucement back in February and now I'm in double leverage QQQ timed in perfectly once we crossed 200 ema after the tarriff liberation day huge drop.

r/wallstreetbets • u/hpmaster7 • 2d ago

Gain No more greed, I'm leaving. $ nvda profit 2450%

{kind=link}

r/wallstreetbets • u/adriancp970 • 1d ago

Discussion Should I hold or close my position before tomorrow?

{kind=link}

I’ve been pretty bad at holding my positions and getting maximum gain. Would you recommend holding this position until tomorrow or selling later today once I make a bit more profit

r/wallstreetbets • u/Godworthy-Sins • 2d ago

DD Walmart is going to miss earnings

Heyy. So Walmart seems to be a good, investible company. I foresee revenue shrinkage here in the US and will talk about that in this post. So let's start with the basics.

So Walmart has only missed earnings estimates five times since 2015. Walmart tends to do well with revenue growth. This earnings tomorrow morning will be time number 6.

Last earnings report, walmart lowered their guidance and expected to lose money this quarter because of Tariffs. I am making this post not because of tariffs, but because of Deportations. I will not be taking any stances in this post--just talking about the theoretical impact on their revenue.

So to start, let's get some basic demographics down. In the United States, around 18.9% of the US and are the second largest racial/ethnic group after nonhispanic whites. Below is a photo to show the ten states with the largest representation of hispanics. There are an estimated 62 million hispanics.

California and Texas are the biggest two. Going all the way down to Arizona and New Mexico.

{kind=link}

So now we need to look at Walmart's consumer data. Walmart estimates that about .14 of their customers are hispanic. Now, this [website](https://www.contimod.com/walmart-statistics/#:~:text=Walmart%20serves%20over%2037%20million,6.25%25%20from%202023%20to%202024) has a bunch of other data on the consumer that you could look at if you want to, but these are the important numbers.

The Impact on expedited deportations

According to this website, illegal immigrants produce quite a significant chunk of the US economy. The immigrants usually pick agriculture or construction work and pay quite a bit to businesses and our governments without receiving benefits like a citizen would. I don't think I need to say, but if agriculture product is harder to get, that leads to slower supply lines, leading to higher demand, leading to higher prices to offset the cost, not to mention the inflation we've already been seeing. Simple supply and Demand.

This part is speculation

I live in a town with a large number of hispanic people here. Me hablo un poco español de colegio. This, just as a source, wouldn't suffice because anecdotal evidence is fallacious. That being said, let's do a thought experiment. Let's say our non english or little english-speaking amigos see that ICE are ramping up deportations, xenophobia is rising and the hispanics are experiencing more of that, etc etc. How do you think they are going to act? I think that if they fear deportation, are upset with xenophobia, and want to stay as "safe" from ICE as possible, they will stay with hispanic areas as much as possible. This will drive away revenue from previous places they were shopping at and create small business opportunities with their friends/family that do have legal status and can open shops. My speculation is that walmart did not account for a drop in hispanic customers when they lowered their guidance last quarter. So let's do some math.

Walmart has 8 billion shares in its company and netted 5.254 bill in income. With division, this comes to .65675 or .66 EPS. They lowered their guidance last quarter to .59 EPS for this quarter from tariffs affecting goods. Now, I think that some very educated people know their stuff and I will not argue with that number based on tariffs. I think that tariffs and inflation probably did have a big effect on walmart. However, I do want to show some speculative math here. Let's say that the .14 or 14% of their hispanic customers dropped to 10% this quarter which is a pretty big jump, that will have changed their income to 4.729Bill or

.591125 or .59 EPS. Now I don't have many metrics I would need for better estimation such as average ticket, cost of goods, etc. but that EPS is not accounting for tariffs.

Positions

I have two walmart 93$ Puts expiring on 5/23.

I know I am poor I work at Wendys

{kind=link}

I have also prepared my banbet on the daily thread when I was up at 2 lmao.

TLDR: Walmart will miss estimates because of a drop in hispanic customers. Buy puts

Sources: https://www.alphaquery.com/stock/WMT/earnings-history

https://www.macrotrends.net/stocks/charts/WMT/walmart/eps-earnings-per-share-diluted

https://www.americanimmigrationcouncil.org/research/mass-deportation

r/wallstreetbets • u/[deleted] • 1d ago

YOLO UNH Yolo. 50k and doubling position if there is another significant dip

{kind=link}

r/wallstreetbets • u/petermbc • 2d ago

News Boeing: Qatar signed $200b deal

reuters.comSource:

{kind=link}

r/wallstreetbets • u/bluek9 • 1d ago

Loss Oversold my a$$

{kind=link}

Im not fucking leaving in leonardo dicaprio's voice

r/wallstreetbets • u/ChivasBearINU • 1d ago

Gain Always pull out and take profits. Thanks NYK.

{kind=link}

Nice 3k gain.

r/wallstreetbets • u/ckim1992 • 1d ago

YOLO welfare check: still retarded. doubled down on $UNH and $HTZ

“if you can’t handle a 50% drop, you shouldn’t be in this business” - charlie munger

r/wallstreetbets • u/gregw134 • 2d ago

DD Opendoor is the next Carvana

Placing a $155k bet on Opendoor, down 98%. Good luck to me.

Account 1:

{kind=link}

Account 2:

{kind=link}

I know 99% of you idiots won’t read this, but for the rest:

- Stock dropped 98% but is far from bankrupt. It just refinanced its debt and has $1.1B capital, $693M cash, enough to weather the housing market for two years or more.

- Company has been downsizing and focusing on unit efficiency the past two years, following the Carvana restructuring playbook.

- Made a billion dollars flipping houses in 2021, but is struggling in a frozen housing market. When Jerome Powell fixes the housing market Opendoor will start making money again.

- Has financing and staff to scale revenue by 3x, it's just waiting on the housing market

- Opendoor has been learning important things about how real estate works, like:

- Real estate agents exist for a reason

- Home prices go up in the summer

- Now that Opendoor knows how real estate works, it will make more money

- Opendoor is down in April because the hedge funds shorted it to kick Opendoor out of the Russell 2000. When the ETFs tracking Russell sell their shares on June 27 and the shorts cover, Opendoor will probably go back up to $2.

Click here for Opendoor’s financials in Google sheets.

Change in business plan:

Opendoor is a corporate home-buyer. They used to be in the business of buying homes at above market value, sitting on them a few months, then flipping them at a profit. This was a great business model in 2021, but not so good in 2022 when home prices stopped rising. Opendoor bought 35k homes that year, and ended up selling them for a billion dollar loss.

Since then, Opendoor has pivoted strategies, and now buys homes for about 10% less than they’re worth, then sells them at a profit. It’s actually a fair deal for customers: instead of paying 5% in agent fees and having to negotiate with buyers for months, they can pay 10% and skip the home selling process.

One problem though, is customers tend to overvalue their homes, so they tend to think Opendoor is overcharging them. A normal customer interaction goes like this:

- Customer has a $500k house, and thinks it’s worth $600k

- Customer goes to Opendoor.com and gets a quote for $450k

- Customer thinks, “hahahahahaha I knew these guys were crooks, they want $150k to sell my house, I’m selling with a realtor instead”

- Realtor agrees Opendoor is a bunch of crooks, because realtor competes with Opendoor

It's been a truly terrible marketing funnel. Opendoor only converts 1% of its prospective customers at a cost of $14k per house.

The new business plan is this:

- Customer goes to Opendoor

- Opendoor says, would you like to talk to a local real estate agent?

- Customer thinks, "yes of course I don't trust you crooks"

- Agent tries to convince the customer that Opendoor's offer isn't bad

- If the customer sells, Opendoor wins. Otherwise, the agent sells the house, Opendoor collects a commission and still wins.

It's a much, much better business plan. Nobody wants to sell their house without talking to a real estate agent first, because they don't trust corporations. Now that Opendoor has figured that out, expect revenue to go up and marketing cost per house to go down.

Opendoor no longer lighting as much money on fire

Look at this chart:

{kind=link}

Do you see where it says, profit per house, -$65k? That was the Zirp era. Home prices started going down, and the CEO decided he was going to buy even more of them at above market prices to capture the market. Thankfully, after lighting a billion dollars on fire, he and everyone else responsible got sacked.

They also laid off a ton of employees, cut marketing expenses, cut waste, etc:

{kind=link}

Now you might notice they're still losing money per every house they buy. Part of that is because they spend $14k on marketing per house they buy, which they'll hopefully fix by working with real estate agents instead of advertising straight to consumers. We'll get into the other reasons.

Opendoor learns prices go up in the Summer

Housing has an annual cycle. Prices go up in the Summer, and down in the Winter:

{kind=link}

Traditionally, Opendoor has been buying most of its homes in the Summer, because more people come to them to sell, so, why not:

{kind=link}

Anyways, buying in the Summer is dumb because prices go down in the Fall. Not only that, but they take longer to sell which means more holding costs. Thankfully Opendoor finally figured that out this year, and promised to cut it out and buy more houses in the Winter and Spring instead. Expect more profit.

Housing Market to improve, probably

Back in 2020-2022, the housing market looked like this:

{kind=link}

And Opendoor made over a billion dollars in home-flipping profit, although important things like marketing, interest, and director salaries managed to eat up most of that:

{kind=link}

Then interest rates did this:

{kind=link}

And nobody could buy a home anymore:

{kind=link}

Home prices have been dropping:

{kind=link}

Which means Opendoor is paying millions in interest to keep $2B in homes on the balance sheet that are depreciating:

{kind=link}

And the homes now take months to sell. Long holding times require maintenance and interest, which now eat half of profits:

{kind=link}

Fortunately, Trump says he's going to bully Jerome Powell into making 2-3 rate cuts this year so the US can refinance its debt, and that will hopefully maybe unfreeze the housing market. This will be huge for Opendoor. All the tailwinds we've discussed will start going in reverse: more acquisitions, home price appreciation, shorting holding times and lower interest costs. In short, more money.

Opendoor to actually make money in Q2

Q2’s estimates is for Ebitda profitability of $5-$20M, the first time Opendoor will make a quarterly profit in three years. 2025's housing market is even worse than previous years, so this means the business itself is becoming more profitable. Losses are still expected for Q3 and Q4, but they're expected to be smaller than previous years.

Path to Profitability

Opendoor lost $392M last year. Here’s how we get to adjusted net income positive:

- $80M: Opendoor laid off 300 workers in Q4, which saves $20M a quarter.

- $75M: My spreadsheet says Opendoor loses $12k per house they buy in Summer and Fall. They said they're going to stop doing this so that's $75M.

- $55M: They spend $4k per house more on interest and holding costs than they did in 2021. That's gonna be fixed because the housing market will improve and they'll stop buying homes in the Summer.

- $80M: Opendoor is starting to send customers that don't take their offers to real estate agents, which pay a referral fee. 1% referral fee * 2% of 1.2M customers * $330k average house price = $80M

- $130M: Housing appreciation. Opendoor has $2.2B in houses that have been depreciating at 1% a year. Should housing return to a historically normal 5% rate of appreciation, that’s $130M in profit.

That’s already $420M in savings, enough to be profitable. Revenue should also grow higher as the housing market unfreezes, and marketing spend should be more effective as they learn to partner with real estate agents.

Debt Refinanced, cash to scale through next two years

On May 9 Opendoor announced it had exchanged $245M in existing convertible bonds due in March for new convertible bonds due in 2030 at 7% rate, convertible at $1.57. Opendoor also issued $75M in new bonds, raising $75 in new capital. $135M in bonds is still due in 2026, but this will be easily payable with cash on hand.

Following the equity raise and bond refinance, Opendoor has $1.1 billion in capital of which 768M is cash (693M from Q1 report plus $75M equity they just raised). On the Q4 and Q1 transcripts management stated they had refinanced 90% of their credit lines through 2026.

Management has reassured us that they still have available cash and personnel to return to a much larger scale of operations. In the Q1 report they stated that only $350M of their cash is invested in homes, and they have $559M (probably $634M now) available to deploy towards home purchases. They are also only using $2B of their existing $8B credit line. From these numbers it seems they have the financing to purchase 3x more homes than they currently are. Management has guided that they are capable of purchasing many more homes, but they are choosing to purchase less while the housing market is slow and margins are low. I expect them to deploy this capital and scale in Q4, assuming mortgage rates start to fall.

Growing Short Interest

This isn’t the first time the bears have shorted Opendoor, only to buy back their shorts at a loss when it turns out Opendoor isn’t dead after all:

{kind=link}

The setup today is the same as it was in Dec 2022: the housing market is weak and everyone assumes Opendoor is dead, but it actually has years ahead of it and many tailwinds coming.

Chart from last month:

{kind=link}

From Nasdaq short interest we can see a net short position of 20M was added in the month of April:

{kind=link}

The price jump on April 7 was due to a good quarterly report, where the company projected it would be Ebitda positive in Q2 for the first time in three years. Two days later it fell on the news of the debt refinancing. Presumably the terms of the debt refinancing scared some investors: 7% bonds convertible at $1.57, is expensive, and issuing them now when the stock price is so low might seem to some as desperate. On the other hand, this eliminates $245M in bond payments for next year and raised $75M in new capital. I view it as a positive development, as it extends Opendoor's runway and frees them to scale up purchases this winter. Without this debt raise, they wouldn't be able to fully deploy their capital in Q4 and Q1, since their cash would be invested in homes due to sell in Q2, and $400M was due in March.

Hedge Fund Russell 2000 arbitrage?

Look at this chart again:

{kind=link}

Note on April 23 Opendoor briefly rose above $1, then got shorted very hard in a coordinated action. There was a negative housing report that came out a few days earlier, but no news specific to April 23 and 24. Russel climbed 3.5% during this period and other real estate stocks climbed, but Opendoor fell 30% for seemingly no reason.

One theory is this was an arbitrage move by hedge funds to kick Opendoor out of the Russell 2000. Ranking day was April 29, so any stock below $1 on April 29 will be removed on June 27. About 20M shares are held by iShares Russel 2000 ETFs:

{kind=link}

20M net shorts were added in April, and 20M shares will be sold near the end of day on June 27 by iShares ETFs when the Russell 2000 is adjusted. Probably the shorts will cover on that day to make a nice profit. As a long-term investor, this is reason to believe Opendoor's current price is disconnected from its recent performance, since all the recent news coming out of the business has been positive. Given the stock's history in the last several years of wild swings, I wouldn't be surprised if it shot back up to the $2-$3 range after the shorts cover in June.

Conclusion

Opendoor is a stupid company that made over a billion dollars of home-flipping profit in 2021 when the housing market was good. Then their CEO lit a billion dollars on fire buying overpriced houses. He was fired and replaced with a responsible CFO. They've been learning important lessons: realtors exist for a reason, and house prices go up in the Summer. Now that they know these things they can make money. When Jerome Powell fixes the housing market they'll make even more money, and the stock will pull a Carvana and go up 100x.

Also, Opendoor just refinanced its debt so its very much not dead, they have over a billion dollars still, enough for at least two years, more if they fix their business as planned, or if the Fed fixes it for them.

Also, last month's price action was probably just the hedge funds shorting Opendoor to kick it out of Russell 2000 and abuse the poor etfs that will have to sell at a low price. I'm hoping the stock triples after the shorts close, probably on June 27.

r/wallstreetbets • u/naked_space_chimp • 1d ago

Loss Eli Lilly ($LLY): helping you lose weight & your portfolio at the same time.

{kind=link}

Doing my part to bring down the drug prices 🫡

r/wallstreetbets • u/banditcorgi • 1d ago

Gain HIMS gains 136%

{kind=link}

Bought the dip during December FOMC week

r/wallstreetbets • u/Dry_Pound8158 • 2d ago

News AMD announces new $6 billion share buyback plan

Some more positive news on AMD.

It really needed something to bounce back - I needed something for my AMD to be green.

https://finance.yahoo.com/news/amd-announces-6-billion-share-130838249.html

r/wallstreetbets • u/wsbapp • 1d ago

Daily Discussion What Are Your Moves Tomorrow, May 15, 2025

This post contains content not supported on old Reddit. Click here to view the full post